Hormuz crisis disrupts India LPG market

India’s LPG market faces acute disruption after Hormuz tensions choked supplies, driving price volatility and forcing emergency sourcing measures across the energy chain.

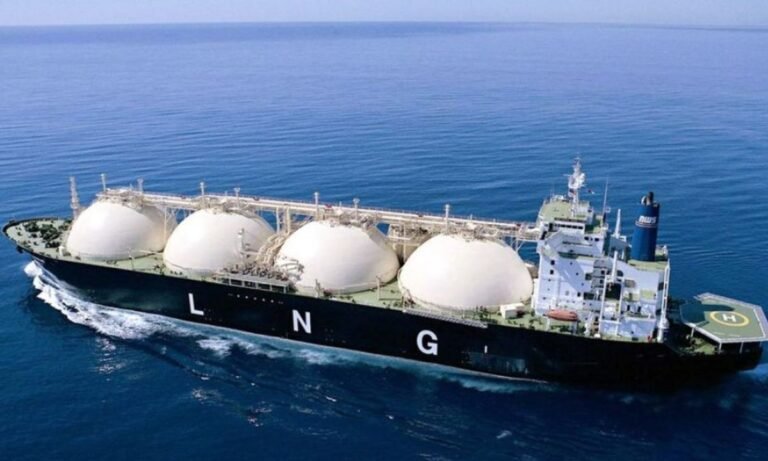

India’s liquefied petroleum gas market has been thrown into turmoil after escalating tensions around the Strait of Hormuz disrupted cargo flows and triggered supply shortages across key importing regions.

The crisis has exposed India’s heavy reliance on Middle Eastern energy routes and forced authorities and companies to scramble for alternative supplies.

The disruption follows heightened geopolitical conflict in the Gulf that has constrained tanker movement through the Strait of Hormuz, a critical artery for global energy trade.

According to the U.S. Energy Information Administration, nearly 20 million barrels per day of oil and a significant share of global LNG transit the strait, with Asia accounting for over 80% of flows. India, the world’s third-largest energy consumer, is among the most exposed importers.

India imports more than 60% of its LPG requirements, with a large portion sourced from Gulf producers such as Saudi Arabia, Qatar, and the United Arab Emirates.

Industry data from India’s Petroleum Planning and Analysis Cell shows LPG demand has grown steadily, crossing 29 million tonnes annually in recent years, driven by household consumption under government-backed clean cooking schemes.

The current supply shock has tightened availability and pushed premiums higher in the spot market. Traders are diverting cargoes, while freight rates have surged due to longer routes and rising insurance costs linked to regional instability.

Market participants report delays in deliveries and increased competition for non-Gulf cargoes, particularly from the United States and West Africa.

The situation marks one of the most severe disruptions to India’s LPG supply chain in recent years. During previous geopolitical tensions, India managed to secure supplies through diversified sourcing, but the scale and immediacy of the Hormuz disruption have created sharper dislocations.

Analysts note that even short-term blockages or slowdowns in the strait can ripple quickly across LPG markets due to limited storage buffers and tight shipping availability.

Domestic implications are already emerging. State-run oil marketing companies are under pressure to maintain stable retail prices despite rising import costs.

India’s government has historically subsidized LPG for lower-income households, and any sustained increase in global prices could strain fiscal balances.

According to India’s Ministry of Petroleum, subsidy spending has fluctuated sharply with global energy cycles, making price stability a politically sensitive issue.

The broader energy system is also feeling the impact. LPG is widely used for cooking, heating, and small-scale industrial applications across India.

Supply disruptions risk pushing consumers toward alternative fuels such as kerosene or biomass, potentially undermining clean energy transition gains achieved over the past decade. The Pradhan Mantri Ujjwala Yojana scheme, launched in 2016, significantly expanded LPG access to rural households, and any supply instability could affect its long-term sustainability.

Global LPG markets were already tightening before the crisis. According to the International Energy Agency, strong petrochemical demand and seasonal consumption patterns had supported prices through early 2026.

The Hormuz disruption has compounded these pressures, amplifying volatility and exposing structural vulnerabilities in supply chains.

Shipping constraints are another critical factor. Tanker traffic through the Gulf has reportedly slowed, while some vessels are rerouting to avoid high-risk zones.

This has increased transit times and reduced effective supply availability. Insurance premiums for vessels operating in the region have also risen sharply, adding to overall import costs.

Read More: LPG Price Reduced for March 2026

In response, Indian refiners and importers are exploring alternative strategies. These include increasing term contracts with non-Gulf suppliers, drawing down inventories, and optimizing domestic production where possible.

However, domestic LPG output meets only a fraction of demand, limiting the effectiveness of internal adjustments.